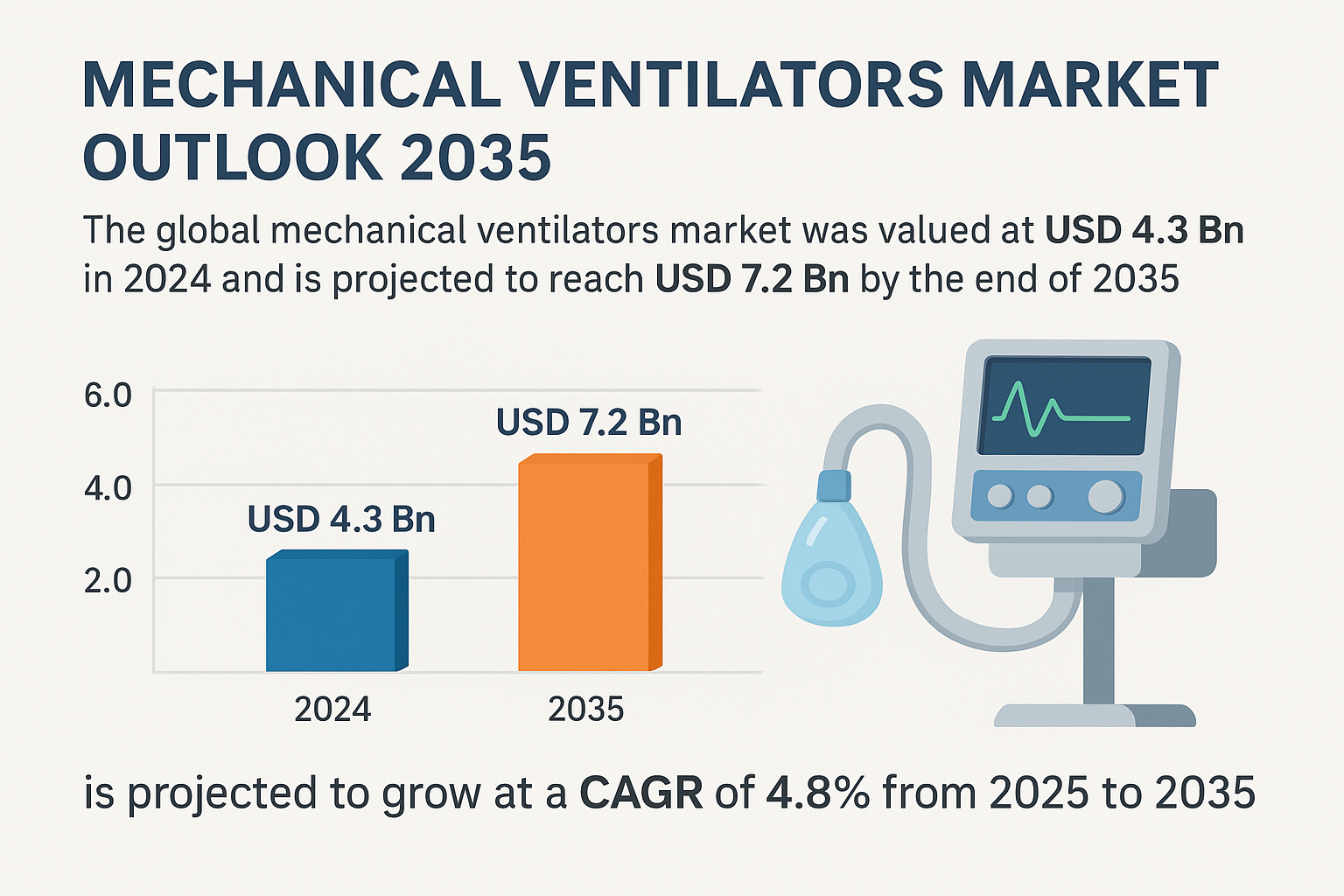

The global mechanical ventilators market was valued at USD 4.3 billion in 2024 and is projected to reach USD 7.2 billion by 2035, growing at a CAGR of 4.8% from 2025 to 2035. The market growth is driven by rising incidences of respiratory disorders, increasing ICU admissions, and growing demand for advanced life-support systems in critical care.

The global mechanical ventilators market is under the dynamic influence of the increased demand for critical care and improvements in emergency preparedness strategies by health systems. Hospitals are expanding intensive care unit capabilities, particularly in developing countries, and are prioritizing ventilation as a basic life-support tool.

Dive Deeper into Data: Get Your In-Depth Sample Now! https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=1397

The global mechanical ventilators market is undergoing a strategic re-orientation, spurred by the interplay of clinical innovation and policy reform. The developing economies are investing into type of tiered healthcare system as well as district level ICU with advanced life-supporting technologies and related medical equipment to care for critical illness in intensive care.

Market Segmentation (2035 Projections)

The market can be segmented across various dimensions, with significant shifts anticipated in the coming decade:

By Product/Service Type (Devices vs. Services)

- Devices Segment Share: The sale of ventilator devices is projected to hold a substantial 61% share by 2035, driven by rapid innovation and fleet upgrades in hospitals.10

By Interface/Mode (Ventilation Type)

- Non-Invasive Ventilation (NIV): This segment is expected to dominate, holding a 53% share by 2035.11 The growth is fueled by the clinical preference for NIV due to greater patient comfort, fewer complications (like ventilator-associated pneumonia), and its suitability for home care settings.12

- Invasive Ventilation: Remains essential for critical care patients with severe respiratory failure or during surgical procedures.

By Product Type/Mobility

- Intensive Care Ventilators (ICU): Expected to be the largest segment, holding an estimated 38% share by 2035.13 This dominance is due to the increasing demand for high-performance, precision ventilators necessary for complex critical care patients who require continuous monitoring and sophisticated respiratory support.14

- Portable/Transport Ventilators: This segment is projected to exhibit the fastest growth, driven by the rising demand for emergency medical services, transport between hospital units, and the increasing shift towards home-based care.15

By Application and End-User

While explicit data for "service type," "sourcing type," and "industry vertical" isn't consistently available as standard market segments in this context, the following application and end-user segments are key:

- Application: Dominant applications include Respiratory Distress (e.g., ARDS), Pneumonia, and management of Chronic Obstructive Pulmonary Disease (COPD).16

- End-User: Hospitals (ICUs & Emergency Departments) remain the largest end-user due to the criticality of the equipment.17 However, the Home Care Settings segment is expected to exhibit the fastest growth as portable devices and telemedicine enable long-term patient management outside the traditional hospital environment.18

Regional Analysis (2035 Projections)

The market growth is geographically diverse, with different regions demonstrating varying paces of expansion:

- North America: Poised to dominate the market, accounting for approximately a 52% share by 2035.19 This leadership is attributed to substantial investment in advanced medical technologies, established critical care infrastructure, and a high prevalence of chronic respiratory conditions like COPD.20

- Asia Pacific (APAC): Anticipated to be the fastest-growing region.21 Growth is propelled by surging healthcare expenditure, rapid expansion of healthcare infrastructure, and the immense burden of respiratory diseases in major economies like China, India, and Japan.22

Market Drivers and Challenges

Market Drivers

- Rising Prevalence of Respiratory Diseases: The increasing global incidence of chronic conditions such as COPD and asthma, particularly in an aging population, is the primary driver for sustained demand.23 For instance, COPD is a leading cause of death worldwide.

- Technological Advancements: Innovation in ventilator design, including Artificial Intelligence (AI) integration, closed-loop ventilation modes (e.g., Adaptive Support Ventilation), enhanced portability, and improved patient-ventilator synchrony, is boosting adoption and replacement cycles.24

- Growing Geriatric Population: Older individuals are more susceptible to severe respiratory illnesses, driving the need for continuous and specialized ventilatory support.25

- Shift to Home Care: The rising preference for non-invasive, portable ventilators for long-term respiratory management at home reduces healthcare costs and enhances patient quality of life.26

Market Challenges

- High Device and Maintenance Costs: The sophisticated nature of advanced ventilators results in high acquisition and maintenance costs, limiting adoption, especially in resource-constrained developing regions.27

- Shortage of Skilled Professionals: The complexity of managing mechanical ventilation requires specialized expertise (e.g., respiratory therapists and intensivists).28 A global shortage of these skilled professionals restricts effective utilization.29

- Regulatory Hurdles: Stringent and evolving regulatory requirements can slow down the introduction of new technologies.30

- Supply Chain Volatility: The market remains vulnerable to disruptions in the supply chain for key components, such as semiconductors.31

Market Trends

- AI and Connectivity Integration: Next-generation ventilators increasingly incorporate AI algorithms for real-time monitoring, predictive analytics, and automated, personalized adjustments to ventilation settings, which improves patient outcomes.32

- Focus on Portability and Multi-Functionality: There is a pronounced trend toward smaller, more rugged, and battery-efficient portable units that can be used across multiple settings (ambulance, home, and ICU).33

- Expansion of Non-Invasive Ventilation (NIV): NIV is rapidly becoming the first-line treatment for many forms of respiratory failure, driving demand for dedicated NIV devices and high-end ventilators optimized for non-invasive modes.

- Value-Based Care: Hospitals are seeking cost-effective solutions by transferring long-term ventilated patients to home care settings, thereby boosting the demand for home-use ventilators.34

Future Outlook

The Mechanical Ventilators Market is poised for strong, sustainable growth, moving beyond the acute, high-volume demand of the pandemic era.35 The future will be defined by smart ventilation ecosystems, where devices are integrated with digital health platforms, enabling remote monitoring and advanced data analytics.36 The primary focus will shift toward enhancing patient comfort, reducing ventilator-associated complications, and expanding access to high-quality respiratory support in decentralized care settings, particularly in the rapidly growing Asia Pacific region.

Buy this Premium Research Report: https://www.transparencymarketresearch.com/checkout.php?rep_id=1397<ype=S

Competitive Landscape

The market is highly competitive, featuring both multinational giants and specialized device manufacturers.37 Competition is focused on technological superiority, clinical efficacy, and strategic expansion into high-growth regional markets and the home care segment.

Key Market Players

- Narang Medical Limited

- Hamilton Medical

- B. Industries

- Noccarc Robotics Pvt Ltd

- Philips

- Fisher & Paykel Healthcare

- Draeger

- Medtronic

- GE Healthcare

- Getinge

- Mindray

- Vyaire Medical, Inc.

- ResMed Inc

- SCHILLER

- Other Prominent Players

Recent Developments

- Market Consolidation: The competitive landscape is currently undergoing a period of realignment and consolidation.45 Notable withdrawals by industry players like Medtronic (exiting the ventilator business in early 2024) and the strategic focus shift of GE HealthCare are creating significant opportunities for other established vendors like Dräger Medical, Getinge, and Hamilton to gain market share.

- Strategic Acquisitions: Companies are strengthening their portfolios through acquisitions. For example, Zoll Medical acquired key product lines from the bankrupt Vyaire Medical (June 2024), significantly enhancing Zoll's position in high-end, neonatal, and transport segments.47

- Product Innovation: Manufacturers are continuously launching products with advanced features, such as new specialist neonatal ventilators and combined function devices that integrate humidification and oxygen therapy.

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

Email: sales@transparencymarketresearch.com