Apple Digital ID: Privacy Concerns & Security Risks

Games |

2025-11-15 03:15:09

Interventional cardiology — the set of minimally invasive procedures used to diagnose and treat heart and vascular disease (angioplasty, stenting, atherectomy, intravascular lithotripsy, structural heart interventions and related imaging/diagnostic tools) — continues to be one of the fastest-evolving segments of medtech. Spending on catheters, stents (especially drug-eluting stents), guidewires, balloons, IVL systems, and advanced imaging/diagnostics is rising as populations age, CVD incidence grows, and clinicians increasingly prefer less invasive alternatives to surgery. IMARC Group+1

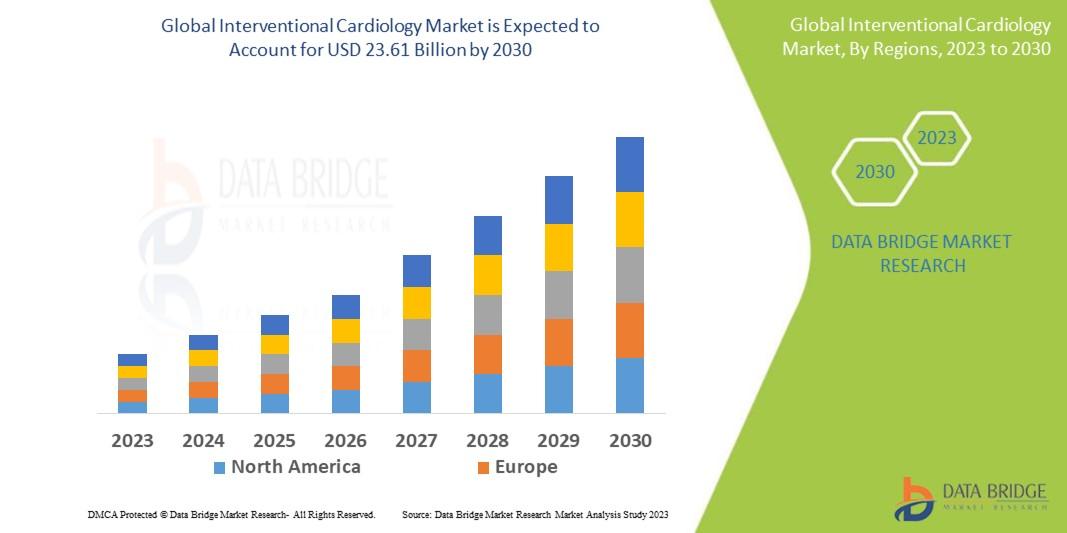

Data Bridge Market Research analyzes that the global interventional cardiology market, which was USD 14.61 billion in 2022, would rocket up to USD 23.61 billion by 2030, and is expected to undergo a CAGR of 7.1% during the forecast period.

Estimates vary by source and by whether the analysis counts only devices used in coronary procedures or includes the broader structural and peripheral interventional markets. Recent figures published by industry trackers show the global interventional cardiology devices market in the mid-teens to low-twenties (USD billions) in the mid-2020s, with projected compound annual growth rates (CAGR) in the ~5–8% range through the late 2020s/early 2030s:

IMARC Group reported a market size of about USD 24.5 billion in 2024, with a forecast to USD 43.2 billion by 2033 (CAGR ~6.5%). IMARC Group

Other analysts place 2024–2025 values between roughly USD 14–19 billion, projecting growth to the high-20s/30s by the end of the decade (CAGRs typically reported around ~6–7%). Differences reflect scope (coronary-only vs. coronary + structural + peripheral) and methodology. Straits Research+1

Rising cardiovascular disease burden & aging populations. Higher incidence of coronary artery disease (CAD), peripheral artery disease (PAD) and structural valvular disease increases procedure volumes worldwide. IMARC Group

Shift to minimally invasive procedures. Surgeons and cardiologists increasingly favor percutaneous approaches over open surgery when clinically appropriate; that raises demand for catheters, stents, and imaging/support devices. Mordor Intelligence

Technological innovation. Improvements in drug-eluting stents, bioresorbable scaffolds (still niche), intravascular lithotripsy (IVL) for calcified lesions, microcatheter technologies, and AI-assisted imaging and navigation are expanding treatable patient populations and improving outcomes. Recent M&A reflects that. MarketWatch+1

Expanding access in emerging markets. Investments in hospital infrastructure and training in Asia-Pacific and parts of Latin America and MEA drive adoption as procedures become more available outside North America and Western Europe. Precedence Research

High device and procedure costs and inconsistent reimbursement in some countries slow adoption.

Regulatory hurdles and time-to-market for novel devices can be lengthy and expensive.

Clinical uncertainty or limited long-term data for some newer technologies (e.g., certain bioresorbables) can restrain uptake. Straits Research+1

By product: coronary stents (drug-eluting stents remain the largest single category), angioplasty balloons, catheters, guidewires, atherectomy/aspiration devices, IVL systems, and structural devices (e.g., TAVR, mitral repair/replacement delivery systems). Coronary stents and catheters typically account for the largest share. Technavio+1

By procedure: percutaneous coronary intervention (PCI) is the largest driver; structural heart interventions (TAVR, transcatheter mitral) are a rapidly growing subsegment with higher unit prices and strong investment. Fortune Business Insights

By end user: hospitals (especially tertiary and cardiac centers) remain the dominant setting, with ambulatory surgical centers gaining traction in some markets.

North America leads in revenue and innovation, driven by procedure volumes, skilled clinicians, and favorable reimbursement. Precedence Research

Europe is a mature market with strong adoption of premium-priced devices and growth in structural interventions. MarketsandMarkets

Asia-Pacific (China, India, Japan, Southeast Asia) is the fastest-growing region due to large patient populations, infrastructure expansion, and rising healthcare expenditure. Precedence Research

Global medtech majors (e.g., Abbott, Boston Scientific, Medtronic, Johnson & Johnson/JNJ) and many specialized players compete across stents, catheters, imaging and adjunct technologies. Strategic activity in the sector has been intense: for example, Johnson & Johnson announced an agreement to acquire Shockwave Medical — a leader in intravascular lithotripsy technology — in a high-profile deal that underscores industry interest in IVL and calcified lesion treatment. That acquisition (announced April 2024) highlights consolidation as companies shore up capabilities across complementary technologies. MarketWatch+1

IVL and calcium-management tools: as an aging patient pool presents more calcified lesions, IVL adoption looks set to grow. MarketWatch

AI and imaging integration: AI-driven imaging, robotic assistance, and improved intraprocedural guidance will create upselling and differentiation opportunities. Fortune Business Insights

Structural heart devices & hybrid procedures: growth in TAVR and transcatheter mitral solutions offers higher margins and new clinical indications. IMARC Group

Emerging markets expansion: lower penetration markets present volume upside if reimbursement and training scale.

Analyst consensus indicates steady mid-single to high-single digit CAGR for the interventional cardiology devices market through the 2020s as technology adoption, demographic tailwinds, and structural procedure growth combine. Exact numbers differ by source and scope, but the broad picture is clear: the market is sizable today and likely to at least double in value across some forecast horizons as higher-value structural and advanced percutaneous therapies become routine. Investors and product teams should watch regulatory approvals, payer coverage decisions, and outcome data for new technologies — these will be the gating factors that determine which innovations scale quickly and which remain niche. IMARC Group+1

Browse More Reports:

Global Offsite Sterilisation Service Market

Global Pressure Relief Devices Market

Global Rice Seeds Market

Global Transparent Food Packaging Market

Global Coronary Artery Bypass Graft Devices Market

Global Lancets Market

Global Potassium Liquid Fertilizers Market

Global Feed Nucleotides Market

Global Sterility Indicators Market

Global N-Propyl Chloroformate Market

Global Rugged Smartphones Sensors Market

Global Automatic Fare Collection System Market

Global Fanconi-Bickel Syndrome Market

Global Systemic Lupus Erythematosus Market

Global Plant-Based Gummy Supplements Market

The global interventional cardiology market sits at the intersection of strong clinical need, rapid technological progress, and active commercial consolidation. For healthcare providers, device-makers, and investors, the coming years will bring both opportunities — via IVL, next-gen stents, AI imaging and structural therapies — and challenges around cost, regulation, and the requirement for robust long-term clinical evidence. Strategic focus on evidence generation, cost-effectiveness, and market access will separate winners from laggards.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com